Copper is having a moment – and not the kind the construction industry was hoping for. Prices for the industrial metal have climbed sharply in recent months, driven by a collision of surging demand from electric grid expansion and a supply chain that was never built to handle it.

The Grid Buildout Is Eating Copper Alive

The math behind copper demand is straightforward: every mile of high-voltage transmission line, every transformer station, every electric vehicle charging hub requires significant quantities of the metal. Governments across North America and Europe have committed to massive grid modernization programs, and those commitments are now translating into real purchase orders hitting the market simultaneously. The result is a demand spike that mining output simply cannot match on short notice.

Grid modernization in the United States alone requires the replacement and expansion of hundreds of thousands of miles of aging transmission infrastructure. The Department of Energy has flagged transmission capacity as a bottleneck for renewable energy deployment, which means utilities are competing aggressively for copper supply just to stay on schedule. Add to that the parallel buildout of EV charging networks, battery storage facilities, and solar farm connections, and the pressure on copper markets becomes easier to understand.

Mining copper is not a fast process. Opening a new copper mine from exploration to production typically takes a decade or more, accounting for permitting, environmental review, infrastructure development, and extraction ramp-up. That timeline mismatch – demand accelerating now, new supply arriving in the 2030s at the earliest – is the core structural problem facing the market. Existing mines are running hard, but they are not running hard enough.

Recycled copper provides some relief. Secondary copper from demolition, electronics recycling, and industrial scrap feeds back into the supply chain and currently accounts for a meaningful share of global refined copper output. Recyclers are doing well in this environment – scrap prices have moved up alongside primary copper prices, and collection operations that were marginal businesses a few years ago are now generating solid returns. But recycled supply alone cannot bridge the gap between current output and projected demand.

Supply Chain Pressure Points Are Multiplying

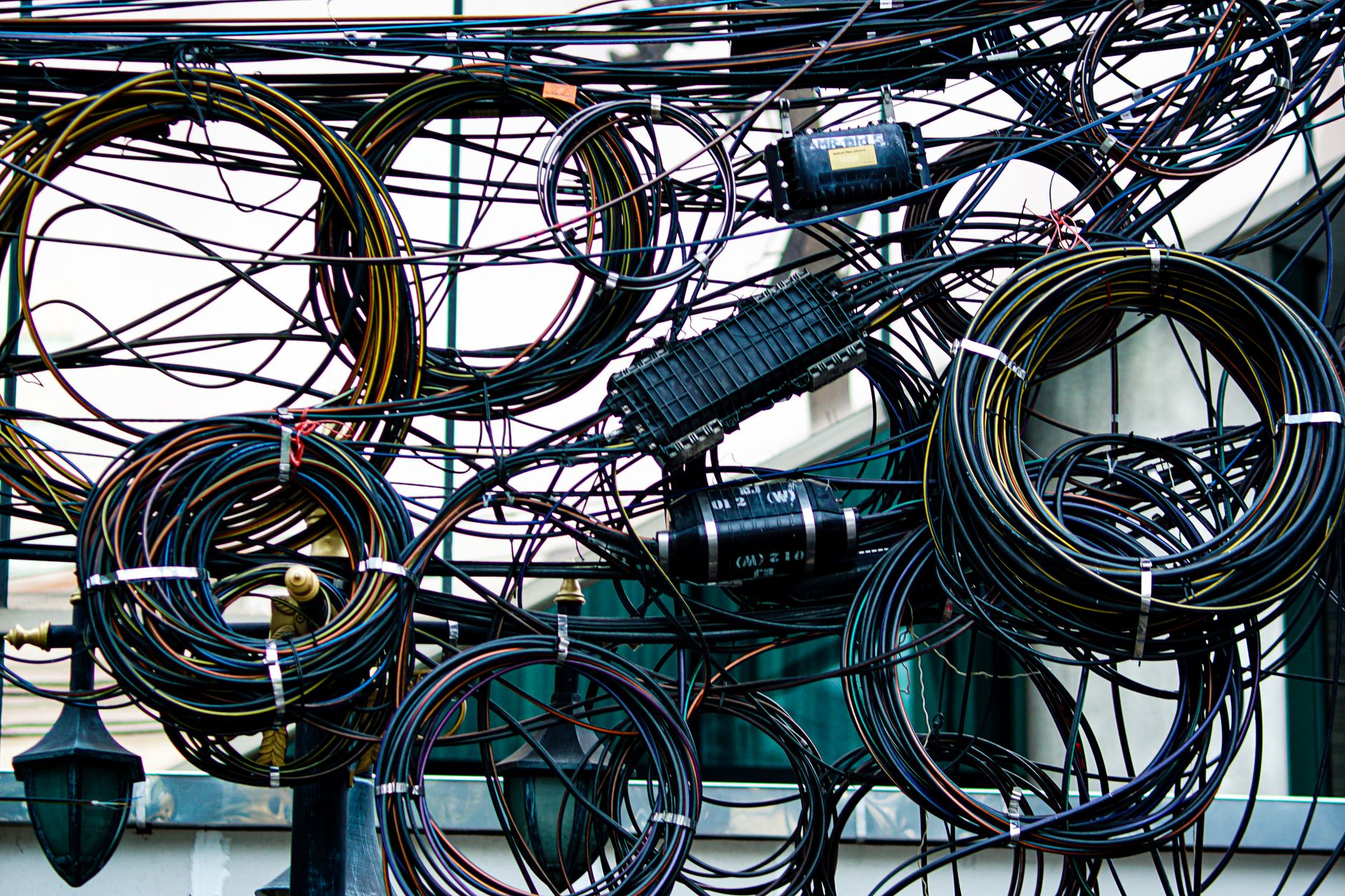

The copper supply chain is getting squeezed from multiple directions at once, and the pressure is not distributed evenly. Wire and cable manufacturers are sitting between two difficult realities: raw material costs are rising faster than they can pass through to customers locked into long-term contracts, while lead times for finished product are stretching to lengths that would have seemed extreme even two years ago. Some utilities report waiting 12 to 18 months for transformer components, a timeline that throws grid modernization schedules into serious doubt.

Chile and Peru together account for roughly 40 percent of global copper mine production, and both countries have faced operational disruptions in recent years – labor strikes, water scarcity issues affecting processing operations, and growing community opposition to mine expansion. The Democratic Republic of Congo, another major producer, operates under its own set of logistical and political complications that add uncertainty to supply forecasts. Geographic concentration of this magnitude means a disruption in any one of these regions lands hard on global prices.

Shipping constraints add another layer of complexity. Copper cathodes moving from South American smelters to North American and European fabricators travel through a global container shipping system that has not fully normalized after years of disruption. Port delays and freight rate volatility have not disappeared – they have become a recurring feature of doing business in physical commodities. Manufacturers that once held lean inventories are now scrambling to build buffer stocks, which itself drives up short-term demand for the physical metal.

Speculative interest in copper futures markets has also intensified. Commodity funds and macro traders view copper as a direct play on the energy transition, and positioning in futures markets has grown considerably. This financial demand does not directly consume physical copper, but it amplifies price moves and can create volatility that makes procurement planning harder for industrial buyers. When futures prices spike, real-world purchase orders either accelerate (buyers locking in supply ahead of further increases) or stall (buyers waiting for prices to pull back), neither of which is good for supply chain stability.

Fabricators – the companies that turn copper cathode into wire, rod, tube, and sheet – are caught in an unusually difficult operating environment. Their customers, particularly in construction and electrical contracting, are pushing back hard on price increases even as input costs climb. Smaller fabricators without the balance sheet to absorb margin compression are starting to struggle. The stress is real enough that it echoes pressures seen in other supply chains where cost escalation is straining smaller operators – a dynamic also playing out, for different reasons, in sectors dealing with rising overhead and input costs across the broader economy.

What This Means for Project Timelines and Costs

The direct consequence for infrastructure projects is cost overruns and schedule slippage. Public utility commissions are reviewing grid expansion budgets submitted just 18 to 24 months ago and finding them significantly underfunded. Private developers building data centers, renewable energy projects, and industrial facilities are facing similar math: the copper bill for a large project has increased materially, and the timeline for getting that copper delivered has stretched in ways that affect financing assumptions and completion guarantees.

Construction contractors have started writing copper price escalation clauses into new project bids – something that was uncommon outside of very large projects before the current run-up. This shifts risk onto project owners, who then push it back up to utilities and governments. Somewhere in that chain, ratepayers and taxpayers absorb the difference. Whether the pace of grid investment slows in response to higher copper costs, or whether governments absorb the overruns and push forward regardless, is the question that copper miners, fabricators, and infrastructure developers are all watching closely right now.