When the Surge Stops

For about two years, inland ports across the country rode a wave of import volume that felt permanent. Warehouses filled. Rail connections expanded. Regional distribution hubs that had spent decades as secondary logistics nodes suddenly became indispensable links in strained supply chains. That volume is now retreating, and the infrastructure built to handle peak demand is sitting underutilized at exactly the wrong moment.

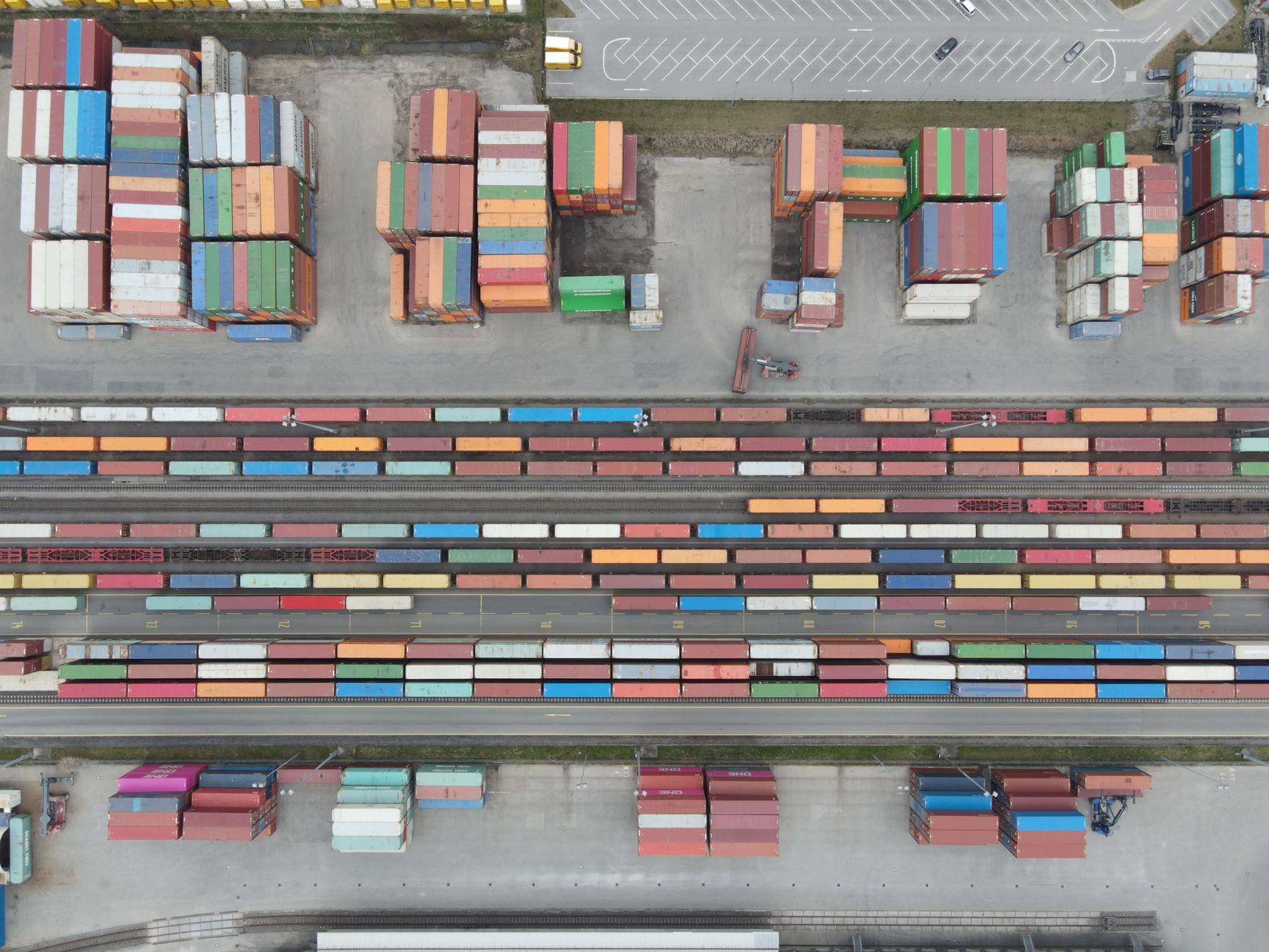

The pullback is not a rumor or a projection. Container bookings out of major Asian export hubs have softened noticeably since late last year, and the effects are working their way inland with a lag that makes the damage easy to underestimate until it is already entrenched. Inland ports – facilities that handle containerized cargo away from coastal terminals, typically connected by rail or truck to seaports – are absorbing the blow in ways that coastal facilities, with their diversified traffic, mostly are not.

How Inland Ports Got Overextended

The logic of inland port expansion made sense during the import boom. Coastal ports like Los Angeles and Savannah were congested beyond their operational limits, and shippers needed somewhere to stage, sort, and store goods. Inland facilities in places like Kansas City, Memphis, Columbus, and the Midwest corridor stepped up. Local governments backed bond financing for expanded rail yards. Private operators added covered storage and cross-docking facilities. Workforce hiring ramped up to meet demand that seemed structural rather than cyclical.

The mistake was treating pandemic-era import volumes as a new baseline. Retailers and manufacturers had spent two years over-ordering to compensate for supply chain uncertainty, building inventory buffers that went well beyond normal operating levels. Once that stockpile cycle completed, import demand dropped back – not to pre-pandemic levels, but closer to them than the expansion plans assumed. Inland ports that sized up for the peak are now running at fractions of intended capacity, carrying fixed costs that were underwritten by projections that no longer hold.

The Economics of Idle Infrastructure

Fixed costs are the real problem. An inland port is not like a warehouse lease you can terminate on 90 days notice. Rail spur agreements, bond obligations for facility construction, and long-term operating contracts with labor and equipment providers lock in expenses regardless of throughput. When volume drops by a third, the revenue side compresses while the cost side barely moves.

Smaller inland facilities that serve single-industry regions are getting hit harder than larger multimodal hubs. A facility positioned primarily to serve automotive supply chains or retail distribution has limited ability to pivot its business mix quickly. The larger hubs in Kansas City or Memphis have more routing options and carrier relationships to draw on, but even they are reporting slower dwell times and reduced rail lift counts compared to peak periods.

Trucking rates that were artificially elevated during the supply chain crunch have also corrected sharply. That correction squeezes the regional carriers and drayage operators who move containers between rail yards and final distribution points – a segment of the freight market where small business loan delinquencies have been climbing as revenue per load falls while fuel and insurance costs hold firm. The combination of lower rates and sticky costs has pushed a number of small regional operators into financial stress that shows up in delayed equipment maintenance, reduced headcount, and in some cases, shuttered operations.

Intermodal rail volume – the category that most directly reflects containerized freight moving through inland ports – posted declines across multiple reporting periods from Class I railroads. That is a concrete operational signal, not an estimate. When rail companies report fewer intermodal loads, the downstream effects on inland port fee revenue are direct and measurable within a single quarter.

What the Regional Workforce Feels

Logistics employment in inland port corridors had become a genuine economic driver for communities that historically lagged in wage growth. Warehouse and distribution center jobs, while physically demanding, offered schedules and compensation that competed with local manufacturing work. The slowdown is reversing some of that gain. Temporary and contract logistics workers were the first to go, but full-time positions have also been eliminated at several facilities as operators try to align staffing with actual freight throughput.

The wage pressure matters beyond individual workers. Local economies in smaller metro areas built retail and housing demand on the assumption that logistics employment would remain at elevated levels. Some of those projections are already off, which creates a secondary drag on local tax revenue and commercial real estate occupancy that takes longer to show up in headline numbers but is already visible to anyone tracking local business closures or apartment vacancy rates.

Where the Adjustment Leads

Some rationalization of inland port capacity was probably inevitable regardless of the current freight cycle. The build-out happened quickly, with less competitive differentiation than the long-term market can sustain. Facilities that invested in genuine operational advantages – faster turnaround times, better technology integration with carrier systems, proximity to high-growth distribution markets – are positioned to consolidate volume as weaker competitors pull back. Those that expanded primarily on the basis of available capital and temporary demand have fewer levers to pull.

The near-term outlook depends heavily on consumer import demand, which is itself tied to retail inventory cycles and broader spending patterns. Retailers who burned through their excess inventory are beginning to reorder, but at more conservative levels and with shorter lead times than the pandemic era. That purchasing behavior structurally reduces the kind of bulk containerized volume that inland ports handle most efficiently.

Some facility operators are exploring alternative revenue by attracting light manufacturing, last-mile logistics operations, or cold storage conversions – uses that can partially fill underutilized space without requiring the scale of a full containerized freight operation. Whether those pivots generate enough revenue to cover the infrastructure debt taken on during the expansion years is an open question that individual facilities will answer differently depending on their local market and how aggressively they financed their growth.

The bond obligations that backed the most aggressive inland port expansions typically run 20 to 30 years. The freight volumes those bonds were structured around assumed continued import growth that the current cycle is clearly not delivering.